2022 in review

Dear readers,

I hadn’t posted anything new to the blog in the latter half of 2022 for various reasons, but another year is in the books and it’s time for the time-honored tradition of another year in review!

On the personal front, I broke my ankle in August, needed surgery followed by physical therapy to walk again, and was out of commission for a couple of months. Thankfully, I have made a full recovery. I’ll post a blog with more details soon.

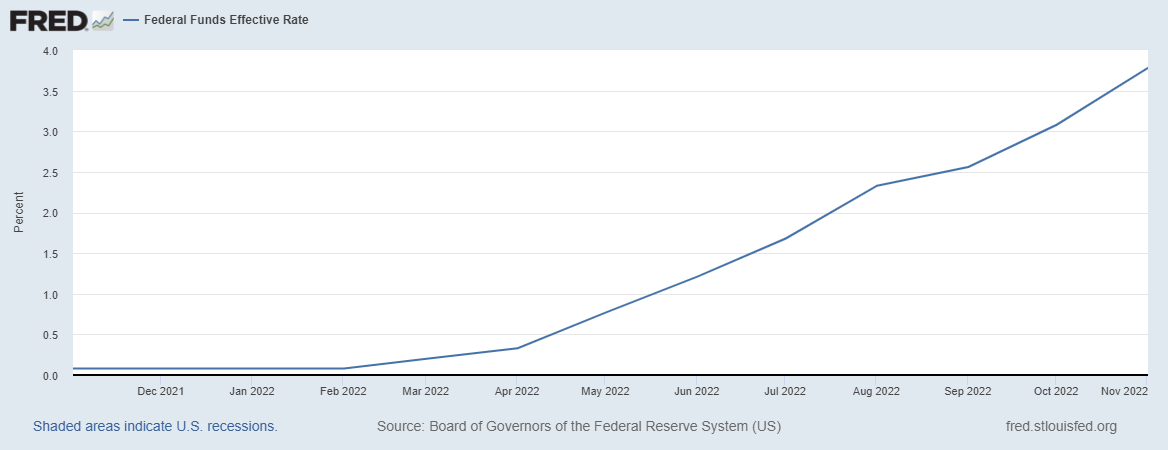

On the financial front, it’s no secret that 2022 was quite disappointing, if not disastrous, for most investors. The Federal Reserve aggressively raised interest rates seven consecutive times in 2022 in an attempt to curb decades-high inflation. After the latest 50 basis point rate hike in December, the target federal funds rate now sits between 4.25% to 4.5%, which is the highest it’s been in 15 years.

The Federal Reserve relentlessly increased the Fed Funds rate in 2022. Image from Federal Reserve Bank of St. Louis.

High interest rates cool off the economy, as it is more expensive to borrow money. This has wide-ranging implications for businesses as well as consumers, and it affects all asset prices including stocks, bonds, real estate, and more. Unfortunately, aggressive rate hikes can also send the economy into a recession.

Furthermore, the world continues to experience disruptions from COVID-19 as well as Russia’s invasion of Ukraine. And cryptocurrencies, the darling asset of 2021, crashed spectacularly. The collapse of FTX exchange, which may well turn out to be the largest financial scandal in history, further fueled this exodus. In 2021, everyone was gushing about cryptocurrency. Today, public sentiment seems to be overwhelmingly negative.

Asset performance

This year might be remembered for many things, but asset performance isn’t one of them.

The S&P 500 index is down -19.44% for the year, after ending up 26.89% in 2021. This represents the largest single year decline since 2008. The bull run of the U.S. stock market, which was basically uninterrupted from 2009 to 2021, is finally over.

The bloodbath in stocks was mirrored by other assets. Bonds are conservative assets used by many investors to generate fixed income and cushion stock market volatility. Unfortunately, bonds took a beating this year as well due to rising interest rates. This might seem counter-intuitive at first, but basically, higher interest rates make existing bonds worth less. The Bloomberg U.S. Aggregate Bond Index, or the “Agg”, returned -13.02% in 2022, marking the worst annual bond returns since the inception of the “Agg” index in 1976. For reference, the previous worst annual return for the bond index was just -2.94% in 1994.

Homes are one of the few assets that held value. The S&P Case-Shiller home price index increased by 7.30% (as of October 2022). Unfortunately, the same has not been true of commercial real estate investments. The FTSE Nareit All Equity REITS index, which tracks all public real estate investments in the U.S., is down -27.46% for the year. This is closely mirrored by many real estate funds; for example, Vanguard’s popular Real estate ETF (VNQ) is down -26.20% for the year.

Things weren’t any better globally. The MSCI ACWI ex-US All Cap index, which covers approximately 99% of all global stocks, excluding the U.S., returned -15.79% (as of November 30, 2022).

As previously mentioned, all major cryptocurrencies fell off a cliff. The massive crypto bull run which started in the summer of 2020 came to an abrupt end in 2022. This article on the promise and collapse of crypto, and its disproportionate impact on minorities, is a great read. Many investors were caught up by the massive hype, the advertisements on TV and social media, the promise of building generational wealth in just a short time, and the fear of missing out.

Bitcoin collapsed in 2022. Chart from Tradingview.com.

Bitcoin, which remains the #1 cryptocurrency by market capitalization, tumbled over 65%. Many lesser “alt-coins” suffered near total collapse.

Finally, inflation remains high, but there are signs that it is finally starting to tame. While Fed rate hikes may continue in 2023, the consensus is that the hikes will slow down, if not stop, before the end of 2023. Recession may be around the corner. But once inflation is under control, the economy will likely need stimulus, and the rate cuts which will follow will almost certainly kick off another bull run. And so the economic cycle continues.

Musings and reflections

I started investing in earnest in 2016, although I certainly remember the dot-com bubble in 2000 and the the global financial crisis in 2007. I was still in school and didn’t have any skin in the game back then. In 2020, there was a brief (but intense) stock market crash and a short-lived recession, which was immediately reversed by massive government stimulus. In retrospect, it felt like that market downturn was over before you could blink. In fact, the S&P had ended 2020 with a gain of more than 15%.

This one feels different, because this is the first major and prolonged market downturn since I started investing. It started 12 months ago and there’s no end in sight. The stuff I previously wrote about market turbulence in May 2022 still holds true seven months later. If previous recessions are any indication, market peak to trough times are measured in years, not months. We still may not have hit the bottom yet, and the market may not bounce back for more years to come.

On the other hand, I am still staying the course and investing as usual. Here are my reasons:

I’m investing for a very long time horizon (decades).

I’m not going to change my behavior to try and match market conditions. Studies have shown over and over again that investors are terrible at this.

Market downturns represent excellent entry points into the market. There’s a tongue-in-cheek saying that the best time to invest was yesterday. We can’t go back in time, but this downturn may well be the best asset accumulating opportunity that current and future investors will ever have.

Not investing is (still) not an option.

Personal finances

Again, as per 2020 and 2021, here is a Sankey diagram of A Frugal Doctor’s household finances for 2022. All values are normalized to 100% of gross income.

We remained relatively frugal and continued to invest most of our take-home income. Unfortunately, investment losses (unrealized) outpaced our investment contributions this year. There isn’t a great way to show negative flow in a Sankey diagram. The bottom line is that our total net worth decreased slightly (by about 2%).

Asset allocation

Not much as changed in terms of overall asset allocation. There was a very minor decrease in U.S. stocks and increase in bonds and international stocks due to the relative underperformance of the S&P 500 in comparison.

Investment holdings

I stayed the course in 2022, so nothing has changed in terms of the funds I actually hold. You can refer to my 2021 in review article for the list of funds I have.

Conclusion

Overall, 2022 was a depressing year for financial markets. The decades-long bull run is finally over. We may enter a recession in 2023. The S&P 500 is down almost 20%. Speculative assets have evaporated. Safer assets like bonds aren’t doing much better. COVID is still around. The Fed seems very hawkish. Inflation is stubborn. And war in Ukraine rages on. Is there any good news?

Remember that historically, the S&P 500 returned approximately 10% compounded annually. This is little consolation to people who are close to retirement, watching their portfolios drop. But at the same time, for those who are lucky enough to have the means to invest, have a long time horizon, and have the discipline to stick to a plan, this current market may well represent the best opportunity for wealth accumulation we will see in a long time. We know today, 15 years later, that the global financial crisis from 2007 - 2009 was an incredible investing opportunity. If history is any guide, the same might be said of the current market downturn in the decades to come. As always, thanks for reading, stay safe and healthy, and have a happy New Year!

Bank failure dominates headlines.